Each year, HEP caucuses with its advisors and executive partners to evaluate the evolving healthcare and growth equity landscape with the goal of determining our investment agenda of ten themes for further exploration. Of these Areas of Focus, we select four for our market sector road mapping exercise. This content was excerpted from our Specialty Pharma: IT and Services sector roadmap. To learn more about our sector roadmaps and other thought leadership initiatives, please contact jlaurash@hepfund.com.

Specialty drugs and therapeutics are at the core of innovation in the healthcare sector as the shift to personalized therapy for complex and rare diseases has grown exponentially in recent decades. Over the past year, the themes of specialty pharmacy services and tools have surfaced time and again in HEP’s discussions with its strategic LP network as key areas of interest within healthcare. These specialty pharma services and solutions seek to improve administrative processes, medication dispensing and adherence, data visibility, care delivery, and clinical outcomes for stakeholders across the specialty pharma ecosystem. Our strategic LPs have highlighted specialty pharma services as key pain points for hospitals and payers given the complexity and high costs associated with coverage and delivery of specialty medicines. The sector is poised to embrace solutions that ensure timely, cost-efficient, and equitable delivery of specialty interventions to patients. Tailwinds supporting growth in specialty pharma spend and new drug development have facilitated an attractive environment for new tools and services helping to drive efficiencies for key stakeholders – we believe this will lead to continued interest and investment in the space.

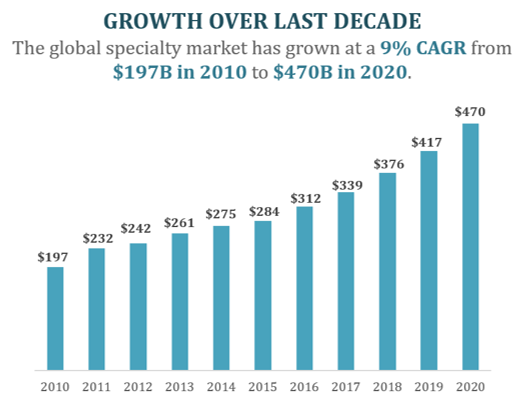

The Rise in Specialty Pharma Spending

The global specialty market grew at a 9% CAGR from $197B in 2010 to $470B in 2020, and is poised to continue to grow with the proliferation of new complex drugs.

This rise in specialty drug spend and development has been driven by an array of factors:

- Well-documented increase in the prevalence of chronic conditions that require specialty therapies, particularly in the context of the United States’ aging population – per the American Hospital Association, the number of Americans with chronic medical conditions is expected to grow by 9% from 2020 to 2030, an increase of 14 million people.

- Industry-wide recognition that specialty drugs reduce long-term costs to the system – payers view the coverage of high-cost specialty drugs as an investment in the health of their members, leading to reduced hospitalizations and cost savings in the future.

- Costs associated with new specialty medications entering the market have been increasing at a rate of upwards of $1 million per year – for example, Hemgenix, a new treatment option for Hemophilia B, is slated to cost upwards of $3.5 million for a single use.

The Need for Specialty Pharma Services & IT

In conjunction with the growth of specialty therapeutics, there has been a paradigm shift in how complex drugs are delivered and paid for. The specialty pharma market is witnessing a transformation marked by a move towards patient-centric care, seamless integration across the care continuum, and advanced site of care management. Both providers and payers have recognized the importance of placing the patient at the center of their delivery models, driving focus on patient satisfaction.

This shift not only aims to enhance patient / member engagement but also seeks to improve clinical outcomes within the specialty pharma ecosystem. In the pursuit of value-based care, novel tools and solutions have become imperative to extract data to validate improvements in outcomes and cost reductions. However, a crucial metric in the value-based care models is time-to-treatment. The prior authorization and patient enrollment processes for specialty drugs can lead to an 8-week lag between diagnosis and the commencement of treatment. In response to this challenge, new solutions are emerging to streamline these processes and expedite time-to-treatment.

These changes present new opportunities for innovative business models and technology, with the potential to further enhance the delivery of specialty therapeutics and improve overall patient outcomes.

Market Tailwinds

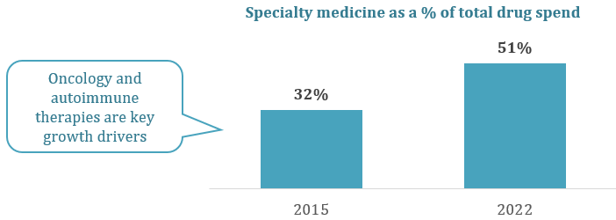

Rising Demand for Personalized Medicine and Targeted Therapies: Patients and providers are increasingly seeking treatments tailored to an individual’s unique genetic makeup, disease profile, and medical history. Advances in genomics and molecular diagnostics have allowed for more precise identification of patient-specific biomarkers and drug targets, enabling the development of highly targeted therapies. This shift towards precision medicine has opened new avenues for the development of tech solutions supporting customized / effective delivery of specialty drugs. In concert with the quest for more personalized treatment options, the need for sophisticated IT solutions and services to manage, track, and administer these therapies will be underscored.

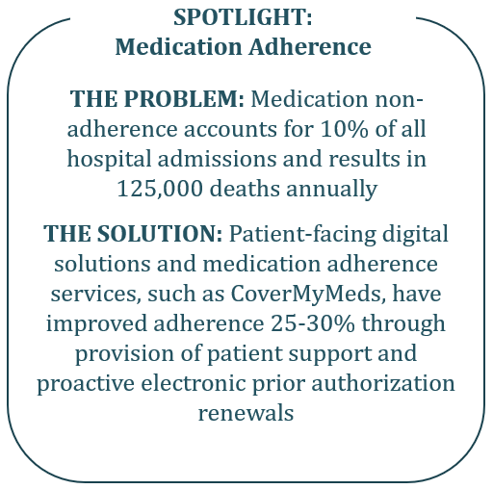

Poor Medication Adherence is Driving Development of Technology Solutions: Affordability challenges and reimbursement complexity, delays in authorization, and inefficiencies in distribution and dispending of specialty medicines has led to low adherence rates and medication abandonment. In 2022, 60% of patients discovered that a prescription was more expensive than expected vs. the prior year, leading 1 in 4 to abandon treatment. This trend of poor adherence has created a compelling market opportunity for technology solutions aimed at enhancing affordability, streamlining reimbursement processes, and improving the overall patient experience within the specialty pharma sector.

Stakeholders Recognize the Need for Technology in Spec Pharma Ecosystem: Payers, specialty pharmacies and other provider organizations, pharma manufacturers, and PBMs recognize the need for improved technology and “connected solutions” to make it easier for patients and other stakeholders to manage their health. Payers view specialty medications as an “investment” in their members’ health to avoid future clinical interventions. As a result, investing in data and tools to support specialty pharma processes will remain a priority.

Shift Towards Lower-Cost Care Settings for Medication Delivery: Stakeholders are increasingly focused on “site of care management” as a means to reduce costs associated with administering specialty medication – it is estimated that administering medication in the physician office setting can reduce costs by up to 50% relative to the hospital setting. Focus on cost reduction via shifting care outside of the hospital requires new tools and solutions to monitor cost savings and, in some cases, facilitate effective care transitions.

Market Headwinds

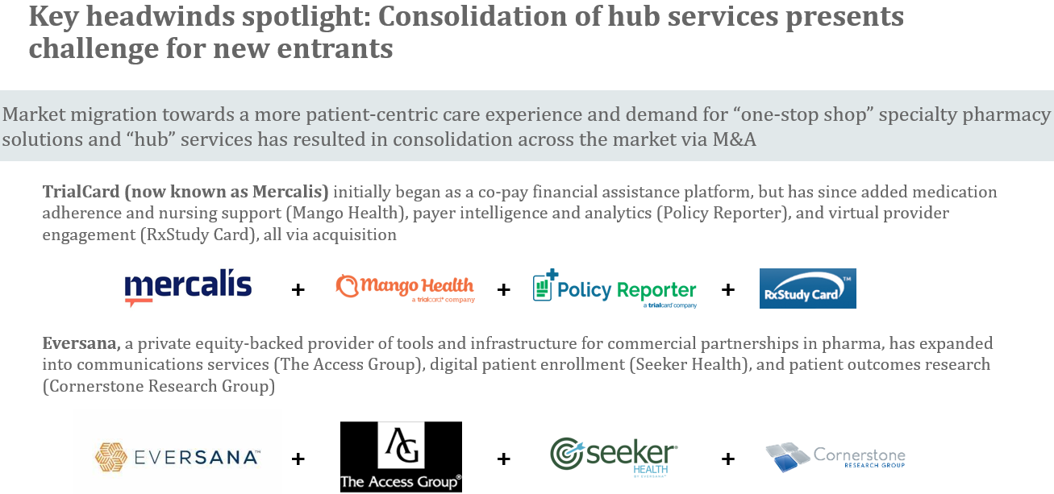

Consolidation and Insourcing of “Hub” Services and Technology Presents Challenges for New Entrants: Hub services providers and technology companies have increasingly sought to become “one-stop shop” solutions for specialty pharma stakeholders, which has led to consolidation by private equity and strategics. Consolidation of hub services providers may make commercial traction harder to come by for new entrants. Further, stakeholders have sought to insource certain functions (via acquisition and organic means) to streamline processes and reduce vendor spend, like Walgreens acquisition of CareMetx.

Potential Impact of Drug Pricing Reform: Drug pricing legislation included in the Inflation Reduction Act of 2022 will allow Medicare to negotiate on with manufacturers directly on prices for certain prescription drugs. Lower revenues for manufacturers may impact budgets for new technologies and services.

Difficulty Defining and Tracking Outcomes in Specialty Medicine: Many factors, including differences in provider care delivery, patient comorbidities and preexisting conditions, as well as medication adherence impact patient response to pharmacotherapy and resulting clinical outcomes. Difficulty in tracking and attributing outcomes and data may hinder the ability of new technology solutions to effectively incorporate data into their workflows.

Lack of Incentive for Pharma Stakeholders to Embrace VBC: Misalignment of incentives in the specialty pharma ecosystem has limited stakeholders from making meaningful investments in VBC. Stakeholders may be reluctant to make investments in new technologies and point solutions focused on enabling VBC as a result.

Implications for Payers:

Payers stand to benefit from the growing number of companies seeking to support the growth of specialty pharma through tools, technologies, and services.

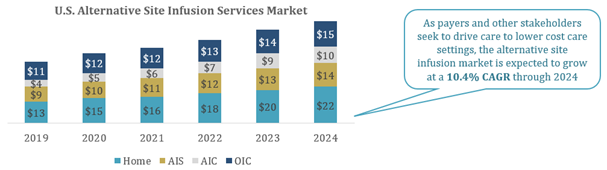

- Alternative site infusion is in the early innings and growing as expansion of providers of infusion therapy in outpatient and home settings is driving cost savings for payers.

- New workflows and solutions improving medication adherence and reducing ab

andonment: Companies focused on creating efficiencies in the benefits verification process will reduce treatment abandonment and improve medical outcomes. - Focus on data benchmarking, patient outcomes, and reporting will improve visibility for payers: Data collection and benchmarking solutions focused on specialty pharma will better equip payers to make reimbursement decisions related to new specialty drugs.

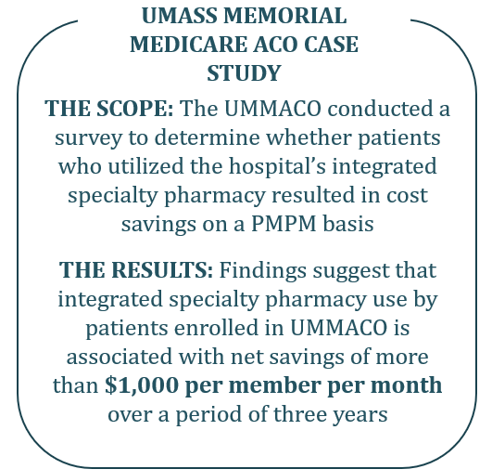

- Growth in integrated specialty pharmacies: Over 90% of large health systems are now operating their own specialty pharmacies in effort to capture a new revenue stream and provide additional services to patients.

- Studies show that the integrated specialty pharmacy model improves patient health outcomes and reduces costs: A study performed by Optum and Shields Health Solutions shows that Medicare Advantage patients filling with a health system specialty pharmacy were associated with 13% lower total cost of care compared to patients filling with an outside pharmacy.

- Growth in integrated specialty pharmacies drives need for technology and support services: With the rise of integrated specialty pharmacies, a need for new technology and services exists to connect health systems with stakeholders and develop new insights.

Market Segmentation

The greater segments of specialty pharma HCIT solutions and pharmacy services can each be broken down into sub-segments which each provide key areas for investment, which are detailed below.

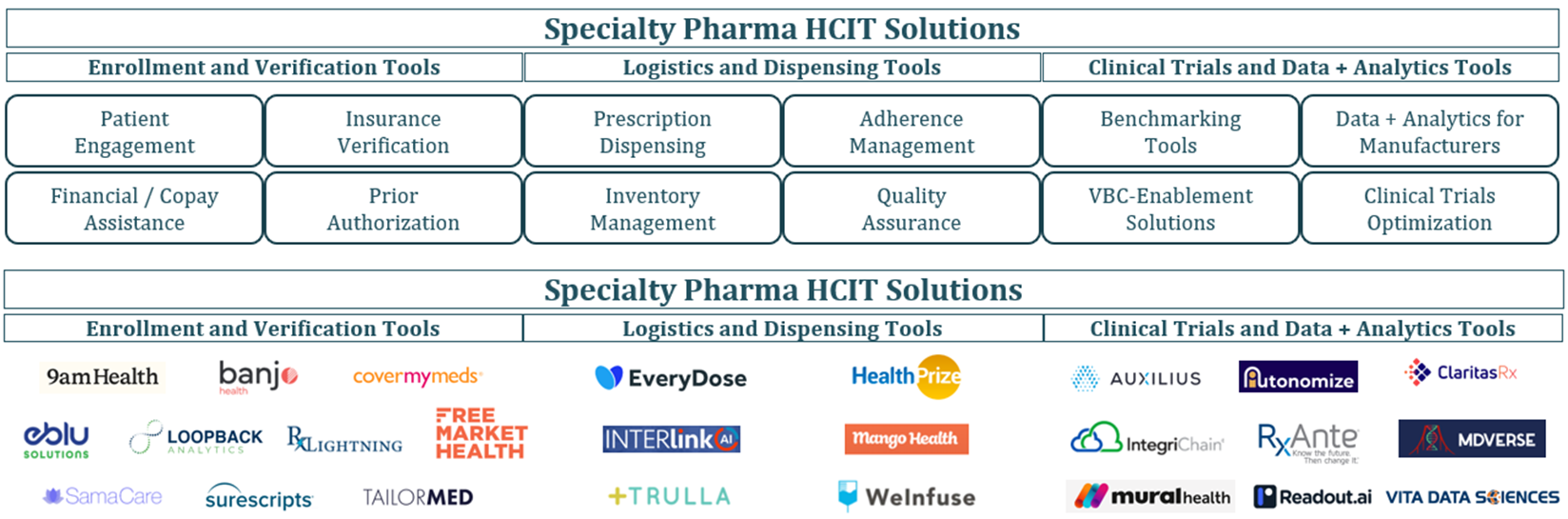

Specialty Pharma HCIT Solutions

HCIT solutions offer three primary sub-segments that are ripe with tech-enabled investment opportunities. First, enrollment and verification tools are becoming increasingly essential in streamlining patient onboarding, ensuring accurate data, and accelerating the time to treatment initiation. Second, logistics and dispensing tools play a pivotal role in optimizing supply chain management and ensuring patients receive their medications seamlessly. Finally, clinical trials and data + analytics tools are at the forefront of innovation, offering robust insights to drive more efficient research and treatment strategies.

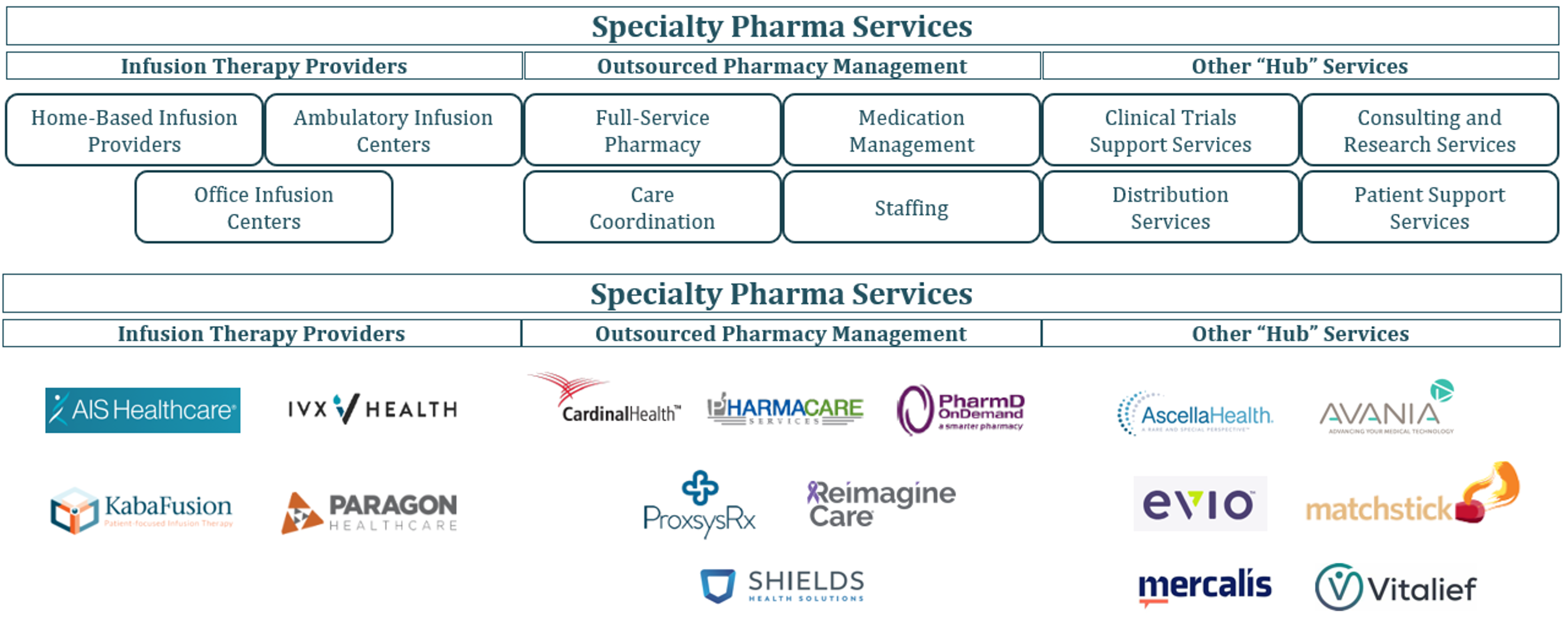

Specialty pharma services, on the other hand, offer a diverse spectrum of care delivery and support, encompassing three main sub-segments: infusion therapy providers, outsourced pharmacy management, and other “hub” services. Infusion therapy providers play a critical role in administering complex medications directly to patients, ensuring precise treatment delivery, and enhancing patient comfort. Outsourced pharmacy management offers pharmaceutical expertise and efficiency, particularly for specialty medications, streamlining the dispensing process and reducing costs. Meanwhile, “hub” services have emerged as a pivotal component of the specialty pharma ecosystem, offering patient support, medication coordination, and data management to ensure therapy adherence and improve patient outcomes. Each of these sub-segments holds its own unique potential for growth and innovation, providing investors with a rich landscape of opportunities to explore and support.

HEP’s Predictions

- While consolidation and insourcing of “hub” services by specialty pharma stakeholders pose challenges for new technology and services vendors, stakeholders remain focused on leveraging technology to improve clinical outcomes, patient experience, and data visibility.

- HEP contends that winners will be determined by their ability to (i) produce a quantifiable ROI in the form of cost reduction through improving medication adherence or reaching vulnerable populations, (ii) address a range of therapeutic areas or indications, and (iii) integrate into existing workflows and infrastructure.

- Technology solutions that facilitate provision of specialty medications in lower cost care settings are particularly well-positioned, as stakeholders are increasingly focused on “site of care management” as a means of reducing costs associated with administering specialty medication.